One of the most common questions in the world of investing is: “How should I invest my 401(k)?”

The process can confusing, and maybe a little scary. How are you supposed to wade through the big menu of choices? How should you allocate the money? This article will provide some clear answers (it’s easier than you might think). Along the way we will borrow the words of Warren Buffett, because not only is he among the greatest investors that ever lived, but he’s also a master at expressing investment wisdom in plain English. Speaking of which, if you come across any terms in this article that you don’t understand, Investopedia.com is a good online resource. The search field at the top of the page provides definitions of common investment terminology.

You’re Doing it Wrong!

Let’s start with an elemental truth about investing: most people do it wrong. In fact, one of the few predictable things about investment management is that the average person is consistently bad at it. Human nature is the enemy of investing. The market looks scary… get out! The market is rocking… all aboard! On average people tend to buy high and sell low, leading to subpar results.

Read up on the Dalbar study for empirical evidence of this phenomenon.

We suggest that you resist that tendency, or maybe take the exact opposite approach.

“You want to be greedy when others are fearful. You want to be fearful when others are greedy. It's that simple.”

- Warren Buffett

The good news is that a 401(k), used properly, and relentlessly, is a very effective accumulator of wealth. And generally speaking 401(k) plans are getting better. Legislative and competitive pressures have driven costs down, and pushed employers to provide high-quality investment options. Still, having a good plan is one thing, using it effectively is another.

Most 401(k) plans are pretty similar when it comes to the menu of investment options. The choices are typically broken down into categories: some stock funds, some bond funds, maybe additional “alternative” categories, and a fixed or money market option. You may want a bit of each, but more on that later. First let’s take a look at the most common mistakes people make when it comes to 401(k) investing:

MISTAKE #1: Not putting enough money in

You have two primary decisions to make when it comes to your 401(k): how much to invest, and how to allocate it. As to the first, the answer is as much as you can, and as early as you can possibly start. You do not need a huge income to create a very sizeable 401(k), but you do need to consistently sock money away over a period of years.

There are plenty of “millionaires next door” out there who amassed significant savings even without the benefit of high incomes. In fact, being a 401(k) millionaire or multi-millionaire is a lottery most American workers can win through patience and smart decision-making.

So, you have committed to saving, right? Now you need to figure out which investment options to pick.

MISTAKE #2: Worrying too much about the fund selection

The good news is that you don’t have to spend too much time trying to figure out which fund on the menu of options is going to be the right investment. It is very difficult, some would argue impossible, to examine a menu of mutual funds and figure out which is going to perform best. So spare yourself the trouble of trying.

“Successful investing starts with humility. Accept that you have no idea what is going to happen in the market in the short-run, and invest accordingly.“

- Warren Buffet (just kidding, Warren didn’t say that, we did, but we are sure he would totally agree!)

If you accept that you won’t be able to pick the best fund, you can turn your attention to the more impactful choice of how to split your money between four different categories:

• Money Market or Fixed account: no fluctuation risk but low returns (although given recent inflationary conditions, rates on such funds can be pretty good at the moment)

• Stocks: highest expected rate of return, most sleepless nights

• Bonds: a somewhat predictable rate of interest, but might not get the job done in terms of funding your retirement

• Alternatives: anything else, these can help diversify risk a bit if available

Thankfully most employers these days (particularly at larger companies) put effort into providing a menu of relatively low cost / high quality funds. And if appropriate oversight is being provided on the plan, you should be ok picking any of the options within a given category. We will talk about how to do that shortly.

MISTAKE #3: Chasing performance, AKA the Morningstar mistake

“In the business world, the rearview mirror is always clearer than the windshield.”

-Warren Buffett

Morningstar publishes the most well-known and widely-followed rating system for mutual funds. 5 Stars for a supposedly great fund, down to 1 Star for a supposedly bad fund. Here’s the rub though: historically the very famous star system has been pretty much useless when it comes to picking funds that will do well in the future. In fact, a study by Vanguard showed that 1 Star funds actually tended to outperform 5 Star funds.

The reason is that Morningstar largely rates funds based on how they did in the past, which does not necessarily tell you anything about how they will perform in the future. In fact, since different investment categories and styles tend to rotate in and out of favor, whatever did well yesterday is often a laggard tomorrow.

That is why the very common approach of looking at the list of funds available in your 401(k) and picking the ones with the highest past performance is not likely to be terribly successful. Better to focus on spreading your money across a variety of categories. When it comes to picking within a category, your best bet might simply be to pick the fund with the lowest internal expenses (something all 401(k) providers are required to disclose these days). When available, index funds are a good way to get low-cost exposure to an asset category.

MISTAKE #4: Attempting to time the market

There are three interrelated aspects to this mistake: underestimating the historical long-term upward trajectory of the market, panicking during corrections, and overestimating your ability to determine the right time to be in or out of the market. Let’s look at them in reverse order.

We thought about bombarding you with statistics that show you can’t tell when to get in and out of the market, but in the interest of brevity (and with the full support of Warren Buffett) we will simply declare: YOU CANNOT TIME THE MARKET.

“We have long thought that the only value of stock forecasters is to make fortune-tellers look good.”

“The stock market is designed to transfer money from the Active to the Patient.”

- Warren Buffett

For further evidence, revisit the Dalbar study referenced earlier… the data shows that those who attempt to time the market experience the worst results of all.

A related problem to attempting to time the market is selling whenever it gets scary. And here’s the thing: it is ALWAYS scary at market lows (aka “the best time to buy”). There is always reason to believe during corrections or crashes that things are going to get worse and worse.

The following comment, or one like it, is something we hear frequently every time the market goes into a swoon: “I’m going to get out of the market and get back in when things calm down.” Allow us to translate that into what it really means: “I am going to sell now while the market is low and buy back in when the market is higher.” That mentality, born of fear, is understandable but kills returns over time.

Remember, prior to retirement you should be a buyer of investments, not a seller. You are accumulating. In that sense, horrible bear markets are the best thing that can happen. In fact, the theoretical ideal would be for the stock market to remain absolutely horrible throughout your working years, only to recover dramatically just before you retire. So instead of fearing bad markets in your working years, embrace the opportunity they represent.

“Look at market fluctuations as your friend rather than your enemy; profit from folly rather than participate in it.”

- Warren Buffett

Other common complaints you hear about the market are that it is either rigged, or it's a casino. Well, it is rigged in the sense that some people have inside information or speedier trading systems, and they are able to take advantage of other players in the market. But if you are long-term buy-and-hold investor, it is hard to have your pockets picked. As far as the gambling aspect, the real difference between the market and a casino is this: with the market the longer you stay at the table the more likely you are to walk away a winner. Take a look at the chart of the stock market shown below. Is the upward trajectory something you really want to bet against? Every day people get up and go to work trying to make their businesses better, that is why stocks tend to rise over time even through difficult periods. The rising trend represents the combined efforts of a lot of smart people working together to innovate and improve companies.

“In the 20th century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. Yet the Dow rose from 66 to 11,497.”

- Warren Buffett

The long-term positive performance of stocks doesn’t do you any good at all if you jump out at the low points. So the amount you put in stocks should reflect how much volatility you can tolerate. Remember, the lows will be SCARY, they always are. Warren offers good advice in this regard as well:

“Unless you can watch your stock holding decline by 50% without becoming panic-stricken, you should not be in the stock market.”

- Warren Buffett

So ask yourself: how much stock are you willing to own, knowing that it could drop in half without scaring you out? With that question in mind, let’s turn our attention to three different approaches to investing wisely in your 401(k).

Target Date Funds: A Popular, Flawed, Effective Strategy

Target Date Funds have exploded in popularity, which might be the best thing that has ever happened to the world of 401(k) investing. Because they are so easy to use they have encouraged more people to contribute to their 401(k)s, a very positive development. We have one major beef with the approach, but for the most part the introduction of these options has been very positive.

The basic idea behind a Target Date Fund is that you start with an allocation based on your expected retirement date (more aggressive if you are far away, less aggressive if you are near retirement), and the allocation gradually becomes more conservative as time goes by. The funds are identified by the year of retirement. So if you expect to retire in 2055, you might look at the “Fidelity Freedom Fund 2055” (the actual name will depend on your plan provider). That fund would start with an allocation of 63% US Stocks, 27% International Stocks, and 10% Bonds. By your retirement in 2055 it would have gradually shifted to 39% US Stocks, 17% International Stocks, 34% Bonds, and 10% Cash.

What we love about target date funds is that they are simple and well-diversified. They are easy to use, and help people avoid most of the common 401(k) mistakes. Our criticism lies with the “one size fits all” asset allocation. In particular, some of the target date funds leave people with too conservative an allocation at retirement. Remember, at age 65 your life expectancy is about 20 years, and you could live well beyond that. Given such a long time horizon many people can’t afford to have a very conservative allocation at retirement. One way to mitigate that is to switch to a date farther out from your actual expected retirement date if you feel the mix is getting too conservative.

In any case, we think Target Date Funds have done a lot of good, and depending on the structure, can be a very solid choice. In some cases, you may have the option to choose among some fixed blends in addition to blends that shift over time. Those can be good choices as well, and mirror the approach we will discuss next.

The Pick-an-Allocation-and-Stick-With-It Approach

This is our favorite, and the one we recommend most often. It takes a bit more effort than using a Target Date Fund, but allows for more customization.

Stocks

First figure out how much stock exposure you can stomach. 100% stock is aggressive of course. Some common alternatives to that are 80/20 (80% Stocks / 20% Bonds), 60/40 (considered “moderate”, this is probably the most common allocation and provides a nice blend of risk and return), 40/60 (starting to get conservative, one of the issues with this being that a bond heavy portfolio may struggle to outperform inflation), and 20/80 (conservative). If you have enough money socked away – a financial plan can help you figure that out – you may be able to go very conservative and still meet your long-term needs. But most people are going to need to stomach the volatility of stocks to get where they want to go financially.

Once you have chosen your stock allocation, you want to break that down into categories: Large Cap (big blue chips), Mid Cap, Small Cap, and International. Some plans with big menus will provide a selection of each, others might skip Mid Cap and just offer Large, Small, and International. It is common to place the biggest allocation in Large Cap US stocks, with smaller allocations in Mid/Small and International. We will provide a sample allocation you can use as a guide. For close to two decades the market has been dominated by Large Cap US stocks due to the enormous profits of leading American tech firms. It’s anyone’s guess whether that will continue in the future. We still think it makes sense to use Large Cap US as the core of a stock portfolio, because that category is made up of many of the best companies in the world. But you may still want to add other categories in the interest of diversification. At the time of this writing International stocks are enjoying a resurgence for the first time in many years… you never know which way the winds will blow next.

Some very deep menus may include categories such as Growth and Value. Growth is made up of fast-growing companies such as those in the tech sector. Value consists of slower-growing but steady businesses whose shares are not priced as expensively. Those styles go in and out of favor at different times, with growth having dominated in recent decades, but value often holding up better in bad markets. You might want exposure to both.

Bonds

Bonds typically provide lower returns and lower volatility (risk) than stocks. In 2022 after a period of extremely low interest rates, inflation spiked and bonds experienced one of their worst markets in history, with the Vanguard Total Bond Index falling more than 13%.

With bonds you invest money and receive a fixed rate of return over a period of years, and then (assuming the issuer doesn’t default) you get your money back. Let’s say you bought a ten-year bond paying 4%, and the next day interest rates spiked higher and a new ten-year bond was available at 5%. Your bond would then be worth less if you tried to sell it, that’s what causes the bond market to fluctuate. However, if you hold to maturity, you still get your money back, so in many cases losses in the bond market are temporary (highlighting their predictability relative to stocks).

Bond funds are typically broken down by the duration, or how long it will take for the bonds in the portfolio to mature. 1-3 year bonds are considered short-term, 4-10 years intermediate-term, and 11-30 years long-term. The longer the bond the higher the yield will tend to be, but also the more susceptible the value will be to fluctuation due to changing interest rates. Mixing short and intermediate-term bonds is a common approach.

In the bond world “High Yield” is code for “junk bonds”. These are bonds with lower credit ratings that pay high rates, but have more risk of default. You might want to keep exposure to this category, if you use it at all, at or below 5%.

Alternatives

Alternatives are the “other” category. These are things that are not stocks, bonds, or cash. Many 401(k) menus do not include alternatives at all. If available, consider adding real estate and commodity positions. Commodities and real estate provide diversification, and can be helpful if inflation becomes a problem. Be aware that the energy sector can be especially volatile.

Cash / Fixed

All 401(k)s have some sort of cash or fixed option. The advantage to this category is that there is no fluctuation. The downside is that the returns are typically below inflation, so even if you aren’t seeing it, your savings in these accounts are actually losing value year after year.

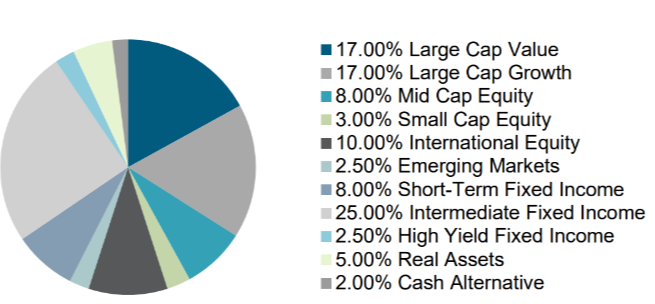

Below is an example of a moderate (roughly 60/40) blend that you can use as a guide. You can visit The American Association of Individual Investors website for additional models to suit varying risk tolerances.

If options like Mid Cap, Real Estate, or Commodities ("real assets") are not available, mix that money back into the stock categories.

So there you have it. Focus on creating a blend based on the categories available in your plan, then stick with that blend and stuff as much money into it as you possibly can. Set it and forget it.

You should choose the “automatic rebalancing” option which will keep your mix in place over time. Also, you may need to tell the system to allocate both your existing balances and your new contributions according to the mix you choose.

A Tactical Approach: 60/40 with Bear Aggression

What if you aren’t content to simply sit still in one allocation? You are compelled to actively manage your plan? Then we will provide a tactical (active) alternative, and we even took the time to give it a cool name.

Do you think you can become perversely happy when the market corrects? Can you watch your account value drop and think “yes, what an opportunity!”? Then this is the strategy for you.

For this approach, you start with whatever blend makes you comfortable. In this example I use 60/40. However, you can just as easily do an “80/20 With Bear Aggression” or even a 20/80. So most of the time you are using your regular allocation, but when the market goes into a correction, when the headlines are screaming “World Chaos!”, when you hear people in your office talking about moving their money under their mattress… GET AGGRESSIVE! At this point you can keep your account allocation the same to stay within your comfort level, but switch future contributions to all stock to take advantage of the lower prices (you might need to turn off auto rebalancing for a while). Not only does this represent sound strategy, but psychologically it may help you to know that even as your account value is taking a hit, you are using the situation to your advantage.

Once the market has recovered you can switch back to your normal allocation (and turn rebalancing back on), confident in the knowledge that you handled the correction better than most other investors in America.

Conclusion

Log in to your 401(k) website today (figure it out, it’s not that hard, or call your HR department for help), and jack your savings rate way up. Then follow the simple advice in this article for the rest of your life, and be happy when the market goes down because you get to buy more stock on sale.

Years from now when you retire comfortably and you’re sitting on a beach somewhere, have a tropical beverage in our (and Warren’s) honor!

"Success in investing doesn't correlate with I.Q. once you're above the level of 25. Once you have ordinary intelligence, what you need is the temperament to control the urges that get other people into trouble in investing."

- Warren Buffett

The information offered is provided to you for informational purposes only. Robert W. Baird & Co. Incorporated is not a legal or tax services provider and you are strongly encouraged to seek the advice of the appropriate professional advisors before taking any action. The information reflected on this page are Baird expert opinions today and are subject to change. The information provided here has not taken into consideration the investment goals or needs of any specific investor and investors should not make any investment decisions based solely on this information. Past performance is not a guarantee of future results and diversification does not ensure a profit or protect against loss. An investment cannot be made directly in an index. All investments have some level of risk, and investors have different time horizons, goals and risk tolerances, so speak to your Baird Financial Advisor before taking action.